Fill Out Your Utah Tc 51 Form

The Utah TC-51 form is a comprehensive document issued by the Utah State Tax Commission, designed to assess whether a company holds a nexus, or sufficient physical or economic presence, within the state that would require it to comply with local tax obligations. Essential for both new and established businesses, the form meticulously gathers details about the company's operations, including their business name, federal ID number, type of business, and the nature of goods or services provided in Utah. Furthermore, it probes into the first and last dates of doing business within the state, customer demographics, and financial activities such as sales and transactions within Utah over the last three years. The questionnaire segments are pivotal for determining the extent of a company's engagement with the Utah market, asking about tangible property, employees or agents performing services, leasing activities, and even the usage of office or warehouse spaces within the state. Moreover, it delves into whether the company solicits orders or maintains goods in Utah, which could influence its tax responsibilities. The TC-51 also serves as a tool for businesses to evaluate their standing under the Streamlined Sales Tax Agreement as a voluntary seller, based on their business activities in Utah. Completing this form with accuracy is paramount, as it concludes with a declaration under penalty of perjury by an authorized officer of the company, emphasizing the importance of the provided information's truthfulness and completeness.

Preview - Utah Tc 51 Form

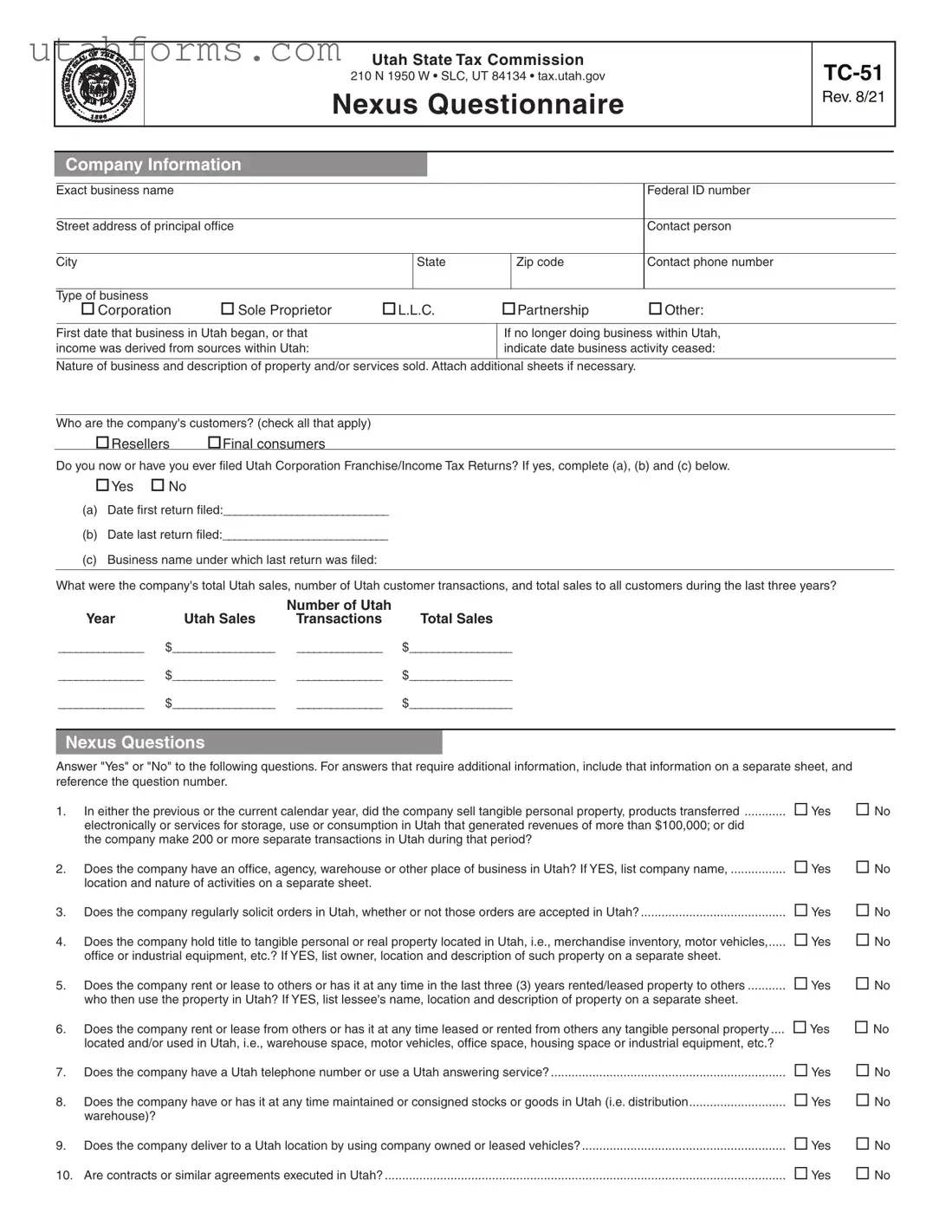

Utah State Tax Commission

210 N 1950 W • SLC, UT 84134 • tax.utah.gov

Nexus Questionnaire

Company Information

Rev. 8/21

Exact business name

Street address of principal office

Federal ID number

Contact person

City

State

Zip code

Contact phone number

Type of business |

|

|

|

|

Corporation |

Sole Proprietor |

L.L.C. |

Partnership |

Other: |

First date that business in Utah began, or that income was derived from sources within Utah:

If no longer doing business within Utah, indicate date business activity ceased:

Nature of business and description of property and/or services sold. Attach additional sheets if necessary.

Who are the company's customers? (check all that apply)

Resellers Final consumers

Do you now or have you ever filed Utah Corporation Franchise/Income Tax Returns? If yes, complete (a), (b) and (c) below.

Yes No

(a)Date first return filed:_____________________________

(b)Date last return filed:_____________________________

(c)Business name under which last return was filed:

What were the company's total Utah sales, number of Utah customer transactions, and total sales to all customers during the last three years?

|

|

Number of Utah |

|

Year |

Utah Sales |

Transactions |

Total Sales |

_______________ |

$__________________ |

_______________ |

$__________________ |

_______________ |

$__________________ |

_______________ |

$__________________ |

_______________ |

$__________________ |

_______________ |

$__________________ |

Nexus Questions

Answer "Yes" or "No" to the following questions. For answers that require additional information, include that information on a separate sheet, and reference the question number.

1. |

In either the previous or the current calendar year, did the company sell tangible personal property, products transferred |

Yes |

No |

|

electronically or services for storage, use or consumption in Utah that generated revenues of more than $100,000; or did |

|

|

|

the company make 200 or more separate transactions in Utah during that period? |

|

|

2. |

Does the company have an office, agency, warehouse or other place of business in Utah? If YES, list company name, ................ Yes |

No |

|

|

location and nature of activities on a separate sheet. |

|

|

3. |

Does the company regularly solicit orders in Utah, whether or not those orders are accepted in Utah? |

Yes |

No |

4. |

Does the company hold title to tangible personal or real property located in Utah, i.e., merchandise inventory, motor vehicles,..... Yes |

No |

|

|

office or industrial equipment, etc.? If YES, list owner, location and description of such property on a separate sheet. |

|

|

5. |

Does the company rent or lease to others or has it at any time in the last three (3) years rented/leased property to others |

Yes |

No |

|

who then use the property in Utah? If YES, list lessee's name, location and description of property on a separate sheet. |

|

|

6. |

Does the company rent or lease from others or has it at any time leased or rented from others any tangible personal property .... |

Yes |

No |

|

located and/or used in Utah, i.e., warehouse space, motor vehicles, office space, housing space or industrial equipment, etc.? |

|

|

7. |

Does the company have a Utah telephone number or use a Utah answering service? |

Yes |

No |

8. |

Does the company have or has it at any time maintained or consigned stocks or goods in Utah (i.e. distribution |

Yes |

No |

|

warehouse)? |

|

|

9. |

Does the company deliver to a Utah location by using company owned or leased vehicles? |

Yes |

No |

10. |

Are contracts or similar agreements executed in Utah? |

Yes |

No |

|

Yes |

No |

|

Yes |

No |

|

Yes |

No |

|

|

|

|

|

|

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

Yes |

No |

17.List names and addresses of employees or representatives, the territory they cover, and designate whether they are employees or independent contractors. Use additional sheets if necessary.

18. Do any of the sales agents in Utah represent your corporation only? |

Yes |

No |

Other Information

19. List the company's three (3) major Utah customers:

20. Are there other types of activities in Utah? Please explain:

SST Voluntary Seller

You are a voluntary seller in Utah under the Streamlined Sales Tax Agreement (see Article IV of SSUTA) if you have met ALL of the following conditions for at least 12 MONTHS PRIOR to registering with Utah:

1.You have had no fixed place of business in Utah for more than 30 days.

2.Less than $50,000 of your property* in located in Utah.

3.Less than $50,000 of your payroll occurs in Utah.

4.Less than 25 percent of your total property* or total payroll*are in Utah.

5.You do not collect sales or use tax in Utah as a condition for you or an affiliate to qualify as a supplier of goods or services to Utah.

6.You are not required to register and collect sales or use tax in Utah as a statutory requirement for yourself or an affiliate to be able to sell, ship or deliver a particular type of product into Utah.

*As defined in the contract between Streamlined Sales Tax Governing Board, Inc and the contractor.

21. Based on the criteria above, are you a voluntary Streamlined Sales Tax seller? |

Yes |

No |

Signatures

Under penalties of perjury, I declare that the information furnished in this questionnaire is, to the best of my knowledge and belief, true, correct and complete. If prepared by a person other than an officer of this corporation, this declaration is based on all information of which you have knowledge.

Name of officer

Title of officer

Signature of officer

Date

Officer's mailing address

City

State

Zip code

Officer's phone number

Name of preparer

Signature of preparer

Date

Preparer's mailing address

City

State

Zip code

Preparer's phone number

File Specifications

| Fact | Detail |

|---|---|

| Form Title | Utah State Tax Commission Nexus Questionnaire |

| Form Number | TC-51 |

| Revision Date | August 2021 |

| Purpose | To determine if a company has a significant connection ("nexus") to Utah for tax purposes. |

| Governing Law(s) | Utah Tax Code and related regulations; Streamlined Sales Tax Agreement for voluntary seller determination. |

How to Write Utah Tc 51

Filling out the Utah TC-51 form is a crucial step for businesses to provide necessary information about their nexus, or connection, with the state. This process helps determine tax obligations to the Utah State Tax Commission. To accurately complete the form, follow the steps listed below:

- Start by entering the exact business name as legally recognized.

- Fill in the street address of the principal office, including city, state, and zip code.

- Provide the Federal ID number of your business.

- Enter the name and phone number of a contact person who the state can reach out to if they have questions.

- Indicate the type of business by checking the appropriate box: Corporation, Sole Proprietor, L.L.C., Partnership, or Other.

- Fill in the first date your business began in Utah or derived income from sources within Utah. Conversely, if applicable, indicate when business activities ceased.

- Describe the nature of the business and the type of property and/or services sold. Attach additional sheets if needed.

- Check who the company's customers are: Resellers, Final consumers, or both.

- Answer whether you have filed Utah Corporation Franchise/Income Tax Returns. If yes, provide the date of the first return, date of the last return, and the business name under which the last return was filed.

- List your company's total Utah sales, number of Utah customer transactions, and total sales to all customers during the last three years.

- Answer the Nexus Questions section by responding "Yes" or "No". Provide additional information on a separate sheet if necessary and reference the question number.

- Complete the section about employee and contract agent information if it applies to your business operations in Utah.

- Under Other Information, list the company's three major Utah customers, describe any other types of activities in Utah, and indicate if you are a voluntary Streamlined Sales Tax seller based on the criteria listed.

- Finally, the form must be signed and dated by an officer of the corporation, and the preparer's information, if someone other than the officer prepared it, should also be included.

Ensuring that all provided information is accurate and truthful is essential, as the signing officer does so under penalty of perjury. Once completed, review the form for completeness and accuracy before submitting it to the address provided at the top of the form or any other communicated submission method by the Utah State Tax Commission.

Frequently Asked Questions

What is the purpose of the Utah TC-51 form?

The Utah TC-51 form, also known as the Nexus Questionnaire, is designed to help determine a company's tax obligations to the state of Utah. By answering a series of questions, businesses can ascertain if they have a "nexus" or a sufficient physical presence in Utah, which would require them to collect and remit sales taxes or meet other tax responsibilities within the state.

Who needs to fill out the Utah TC-51 form?

Any business that conducts operations in Utah or has interactions that could constitute a physical presence in the state should complete the Nexus Questionnaire. This includes, but is not limited to, companies selling tangible personal property, providing services, or having employees or representatives in Utah.

What information is required on the TC-51 form?

The form requests detailed information about the company, including the exact business name, principal office address, federal ID number, and contact details. It also asks for specifics about the type of business, the nature of business activities in Utah, and a history of the company's sales and transactions in the state. Additionally, businesses must answer questions regarding their physical presence, employees, and property in Utah.

What qualifies as "doing business" in Utah for the purposes of this form?

"Doing business" in Utah encompasses a variety of activities, such as generating sales or income from within the state, holding inventory or owning property, leasing property to others for use within Utah, and employing staff or representatives who operate within the state. Further examples include soliciting orders, having an office, or providing services in Utah.

How does a company determine if it has a nexus in Utah?

Through the Nexus Questionnaire (TC-51), a company evaluates its activities against the criteria outlined by the Utah State Tax Commission. A nexus can be established through physical presence, such as owning property or having employees in Utah, or through economic actions, like reaching sales thresholds. Specific questions within the form guide companies in assessing their nexus status.

What happens if a business does not complete the TC-51 form?

Failure to complete the TC-51 form when required can lead to unintended tax compliance issues. If the Utah State Tax Commission determines that a business has a tax obligation that hasn't been met, the company may face penalties, interest on unpaid taxes, and back taxes for the period of non-compliance.

Can a business be considered a "voluntary seller" under the form's guidelines?

Yes, a business can qualify as a voluntary seller under the Streamlined Sales Tax Agreement (SSUTA) if it meets certain criteria, such as not having a significant physical presence in Utah or engaging in activities that would not establish a substantial nexus. This status allows the company to collect sales taxes in Utah voluntarily without being mandated by a physical presence.

Where can a business file the Utah TC-51 form?

The completed TC-51 form should be submitted to the Utah State Tax Commission. Businesses can mail it to the address provided on the form or check with the Tax Commission for any available online submission options or additional filing instructions.

What should a company do if its nexus status changes after submitting the TC-51 form?

If a company's business activities change in a way that affects its nexus status in Utah, it should update its information with the Utah State Tax Department accordingly. This might involve submitting a new Nexus Questionnaire or contacting the Tax Commission to inform them of the changes, ensuring compliance with state tax laws and regulations.

Common mistakes

When filling out the Utah TC-51 form, which is critical for companies operating within or having ties to Utah, there are common mistakes to be aware of. This is more than a mere formality; the information provided can have significant implications for a company's tax obligations and legal responsibilities in the state of Utah. Let's delve into five typical errors that can trip up even the most diligent of businesses.

Not Providing Complete Company Information: The form begins with a request for basic yet crucial details about your business. Oftentimes, companies might overlook or incorrectly fill out their exact business name, federal ID number, or the principal office address. It's essential to double-check this section to ensure that all the information matches your official records. Any discrepancy here can lead to confusion or delays in processing.

Incorrect Type of Business Designation: Selecting the correct type of business entity is more important than it might appear at first glance. Whether your business is a Corporation, Sole Proprietor, LLC, Partnership, or falls into the "Other" category has significant legal and tax implications. An incorrect selection can misrepresent your business to the Tax Commission, potentially leading to incorrect tax assessments or obligations.

Failure to Specify Nature of Business or Services Sold: A vague description (or a lack thereof) of your business and the goods or services it provides can be a red flag. This section helps the tax authorities understand the scope of your operations and assess nexus properly. Especially for businesses that operate in multiple sectors, providing clear and detailed information is crucial. Attaching additional sheets for a comprehensive explanation is recommended if the space provided is insufficient.

Overlooking Nexus Questions: The nexus questions are designed to determine if your business activities establish a tax obligation to the state of Utah. Answering "Yes" or "No" without due consideration or failing to provide required additional information can lead to compliance issues. These questions encompass a wide range of activities, from selling tangible property in Utah to renting or leasing property. It's imperative to carefully review these questions and provide thorough answers.

Incorrect or Incomplete Sales and Transactions Reporting: When reporting Utah sales, transactions, and total sales, accuracy is key. Estimations or rounding off figures can lead to inaccuracies in tax reporting and possible audits or penalties. Ensure that the sales and transactions are reported accurately, reflecting the true extent of your business dealings in the state over the specified period.

Avoiding these mistakes requires careful attention to detail and an understanding of your business's operations within Utah. When in doubt, consulting with a tax professional or legal advisor can ensure that the TC-51 form is completed accurately and thoroughly, minimizing the risk of errors and ensuring compliance with Utah's tax laws.

Documents used along the form

When working with the Utah TC-51 form, which helps the Utah State Tax Commission assess a company's tax responsibilities related to doing business in Utah, various other documents and forms often play crucial roles in ensuring compliance and thoroughness of tax reporting. These documents complement the TC-51 by providing additional details about the company's activities, representatives, and financial specifics in Utah.

- Form TC-20: This is the Corporation Franchise or Income Tax Return form. It's essential for corporations operating within Utah, as it reports income, calculates the tax liability, and covers payment details. Companies need to provide comprehensive income statements and balance sheets alongside this form.

- Form TC-40: Known as the Individual Income Tax Return. Although primarily for individuals, Sole Proprietorships in Utah might need to include this with their filing to report personal income derived from their business activities within the state.

- Form TC-160: This is the Credit for Income Tax Paid to Another State form. For businesses operating in multiple states, this form helps to avoid double taxation on income by allowing a credit for taxes paid to other states.

- Worker Verification Forms: Employers in Utah are required to verify the legal work status of their employees. This involves completing Form I-9 for each employee and may include supporting documents like E-Verify confirmation.

- Form TC-547: The Notice of Change for Business and Employment Taxes form is used when a business needs to update its information related to tax accounts, including changes in ownership, address, or business status.

- Power of Attorney (POA) Forms: A POA is necessary when a business wishes to authorize another individual, such as a tax professional, to discuss and handle their tax matters with the Utah State Tax Commission on their behalf.

These documents, when used alongside the Utah TC-51 form, provide a comprehensive snapshot of a business's tax profile, ensuring that all relevant activities are accurately reported and any applicable taxes are correctly calculated. Businesses may need to consult with a tax professional to ensure that they are filing all required forms and documents correctly and taking advantage of any available tax benefits.

Similar forms

The Utah TC-51 form is closely related to the Multi-State Tax Commission (MTC) Nexus Questionnaire. Both documents are designed to determine a company's tax obligations based on their activities within a specific state or across multiple states. The questions focus on the presence of physical or economic connections (nexus) that may subject a company to state taxes, including whether the business has a physical location, employees, or substantial sales within the jurisdiction.

Similar to the Utah TC-51, the California Form 3834, Interest Computation Under the Look-Back Method for Completed Long-Term Contracts, also assesses business operations, but with a more specific aim. It calculates the interest due or to be refunded under the look-back method for income realized on long-term contracts. This form examines the timeline of income recognition and the resulting tax implications, highlighting the importance of accurate financial reporting and its impact on tax obligations.

The New York State ST-100 Form, Quarterly Sales and Use Tax Return, shares similarities with the TC-51, in that it gathers details about a business's sales activities within the state. It requires businesses to report the total sales, taxable sales, and the amount of sales tax collected or owed. Both forms help state tax authorities determine the extent of a company's tax liability based on its operations and sales within the state.

The Texas Franchise Tax Public Information Report (Form 05-102) is another document akin to the Utah TC-51. It collects detailed information about a company's structure, ownership, and management for tax purposes. The focus is on understanding the entity’s organization and activities to accurately assess its franchise tax obligations, underlining the correlation between business operations and tax liabilities.

Florida’s Annual Resale Certificate for Sales Tax (Form DR-13) parallels the Utah TC-51 by requiring businesses to disclose information about their resale activities. While the Utah form seeks to ascertain a broad nexus with the state for various tax purposes, the Florida certificate specifically addresses sales tax exemptions for goods purchased for resale, centering on how businesses interact with tax regulations regarding their sales activities.

The Virginia Nexus Questionnaire is directly comparable to Utah’s TC-51 form, as both are designed to establish a business’s connection to the respective state for tax reasons. They inquire about physical presence, employee activities, and sales within the state to determine if the entity meets criteria that necessitate state tax collection and payment, demonstrating the states’ efforts to tax businesses fairly based on their in-state economic activities.

Illinois Business Registration Application (Form REG-1) serves a similar purpose to the Utah TC-51 by collecting information about a business to determine its tax responsibilities in the state. While the REG-1 is more focused on initially setting up tax accounts for various state taxes, both forms require detailed disclosures about the company’s activities, structure, and identity, laying the groundwork for ongoing tax compliance.

Colorado Sales Tax/Wage Withholding Account Application (CR 0100AP) is designed to register a business for tax purposes, similar to how the Utah TC-51 identifies tax obligations based on nexus. This form captures key details about the business to ensure accurate tax collection, especially for sales and payroll taxes, underscoring the relationship between business operations and tax responsibilities.

The New Jersey Business Registration Application (Form NJ-REG) also mirrors the intent behind the Utah TC-51 form. It collects comprehensive information on a business to establish its identity and operational scope within New Jersey, facilitating appropriate state tax registration and compliance. By detailing the nature and extent of business activities, both forms help delineate tax obligations accurately.

Lastly, the Alabama Business Privilege Tax Return and Annual Report (Form PPT) is akin to Utah’s TC-51 in that it assesses a company’s exposure to state-level taxes. However, it specifically addresses the privilege tax, which is based on the entity’s net worth and business activities in Alabama. This form, like the TC-51, underscores the principle that a business’s operations and financial health are crucial determinants of its tax liabilities in a given state.

Dos and Don'ts

When dealing with the Utah TC-51 form, it's crucial to pay attention to the details. This document, which the Utah State Tax Commission uses to understand a company's nexus within the state, requires accurate and thorough information. Below, find a list of do's and don'ts to help guide you through the process:

- Do read through the entire form before starting to fill it out. This will help you understand what information is required and ensure you have all necessary details at hand.

- Do provide exact information for your business, including the correct federal ID number, the exact business name, and accurate contact details. Misinformation can lead to delays or issues with your form's processing.

- Do check all the boxes that apply to your business under the company information and nexus questions sections.

- Do attach additional sheets if necessary, especially when explaining the nature of your business and providing descriptions of property or services sold. Make sure to reference the question number on these attachments.

- Do sign and date the form at the bottom, verifying that the information provided is true, correct, and complete to the best of your knowledge.

- Don't leave any sections blank. If a question does not apply to your business, indicate this with a "N/A" or "None" to demonstrate that the question was not overlooked.

- Don't forget to review your form for errors before submitting. This includes checking for accurate calculations, correct dates, and ensuring that all necessary sections have been completed.

By following these guidelines, you can ensure a smoother process in completing and submitting the Utah TC-51 form. Remember, providing accurate and complete information is key to complying with the Utah State Tax Commission's requirements.

Misconceptions

When it comes to understanding the Utah TC-51 form, also known as the Nexus Questionnaire, there are several misconceptions that can lead to confusion or incorrect assumptions. It's important to clarify these points to ensure accurate and compliant completion of the form.

Only for large businesses: Some may think the TC-51 form is only required for large corporations. However, any company, regardless of size, that has business activities in Utah which may establish a tax nexus is required to complete the form. This includes sole proprietors, partnerships, and LLCs, not just large corporations.

Physical presence is necessary to file: Another common misconception is that a company must have a physical presence in Utah to need to fill out the TC-51. In today's digital age, economic activities such as making sales or transactions in the state can also establish nexus, requiring the form's completion.

One-time completion: Some businesses believe that once they submit a TC-51 form, they do not need to file it again. However, if a company's business activities in Utah change, they may need to submit an updated form to reflect the current nature of their business and activities within the state.

For tax payment purposes only: There's a misconception that the TC-51 is used to pay taxes or that completing it means a company owes taxes. The form primarily serves to determine a company’s tax nexus with Utah. Actual tax liabilities are assessed and paid separately, based on the nexus established.

Only for disclosing financial data: While the form does require financial information like Utah sales and transactions, it's also designed to gather information about the nature and extent of a company's business activities in Utah. This includes employee activities, property ownership, and more, not just financial data.

It replaces other tax documents: Companies might think that once they fill out the TC-51 form, they don’t need to complete other state tax documents. The truth is, this form is just one part of broader tax compliance requirements in Utah. Based on information provided in the TC-51, additional filings may be necessary.

Understanding these points can help companies accurately determine their nexus status and comply with Utah's tax laws.

Key takeaways

The Utah TC-51 form is an essential document for companies engaged in or planning to engage in business activities within the state of Utah. Understanding its components and requirements is crucial for proper compliance with state tax regulations. Here are eight key takeaways to guide individuals and businesses in filling out and using the Utah TC-51 form:

- Company Information is Essential: Initially, the form requires comprehensive information about the company, including the exact business name, principal office address, federal ID number, and contact information. This ensures that the state tax commission has accurate records for correspondence and verification.

- Business Type Identification: Identifying the type of business (Corporation, Sole Proprietor, L.L.C., Partnership, or Other) is mandatory. This classification helps in the determination of tax obligations and applicability of specific tax conditions relevant to the entity's operational structure.

- Operational Timelines: The form queries about the initiation or cessation dates of business activities within Utah. Providing accurate dates is crucial for determining the time frame of tax liabilities and responsibilities.

- Nature of Business and Clientele: Companies must outline the nature of their business, the kind of property and/or services sold, and identify their primary customers (resellers or final consumers). This information assists in evaluating the company's tax nexus and potential sales and use tax collection obligations.

- Tax Filing History: For companies that have previously filed Utah Corporation Franchise/Income Tax Returns, details about the initial and latest filings are requested. This historical data is important for the tax commission to assess ongoing compliance and tax status changes.

Disclosure of activities performed by employees, sales representatives, or independent contractors within Utah is vital. This helps in the assessment of nexus and the determination of tax collection duties based on the presence and activities of personnel. - Voluntary Seller Status: The form clarifies eligibility for voluntary seller status under the Streamlined Sales Tax Agreement, based on the absence or minimal physical presence and economic activities within Utah. Companies meeting certain criteria can qualify as voluntary sellers, impacting their tax collection and remittance responsibilities.

- Verification and Certification: The concluding section of the form requires the signature of an authorized officer and the preparer, attesting to the accuracy and completeness of the information provided under penalties of perjury. This affirmation underscores the legal responsibility to furnish correct data and comply with state tax regulations.

Proper completion and submission of the Utah TC-51 form are integral for any business operating in or engaging customers within Utah. It aids in the accurate assessment and fulfillment of tax obligations, ensuring compliance with state laws and regulations.

Common PDF Templates

Dws Forms - Details on the significance of providing accurate employee wage details to the Utah Department of Workforce Services.

Medical Power of Attorney Form Utah - The directive affords peace of mind, not just for you but also for your family, by clearly documenting your health care preferences and reducing the burden of making difficult decisions.