Fill Out Your Utah Tc 41 Form

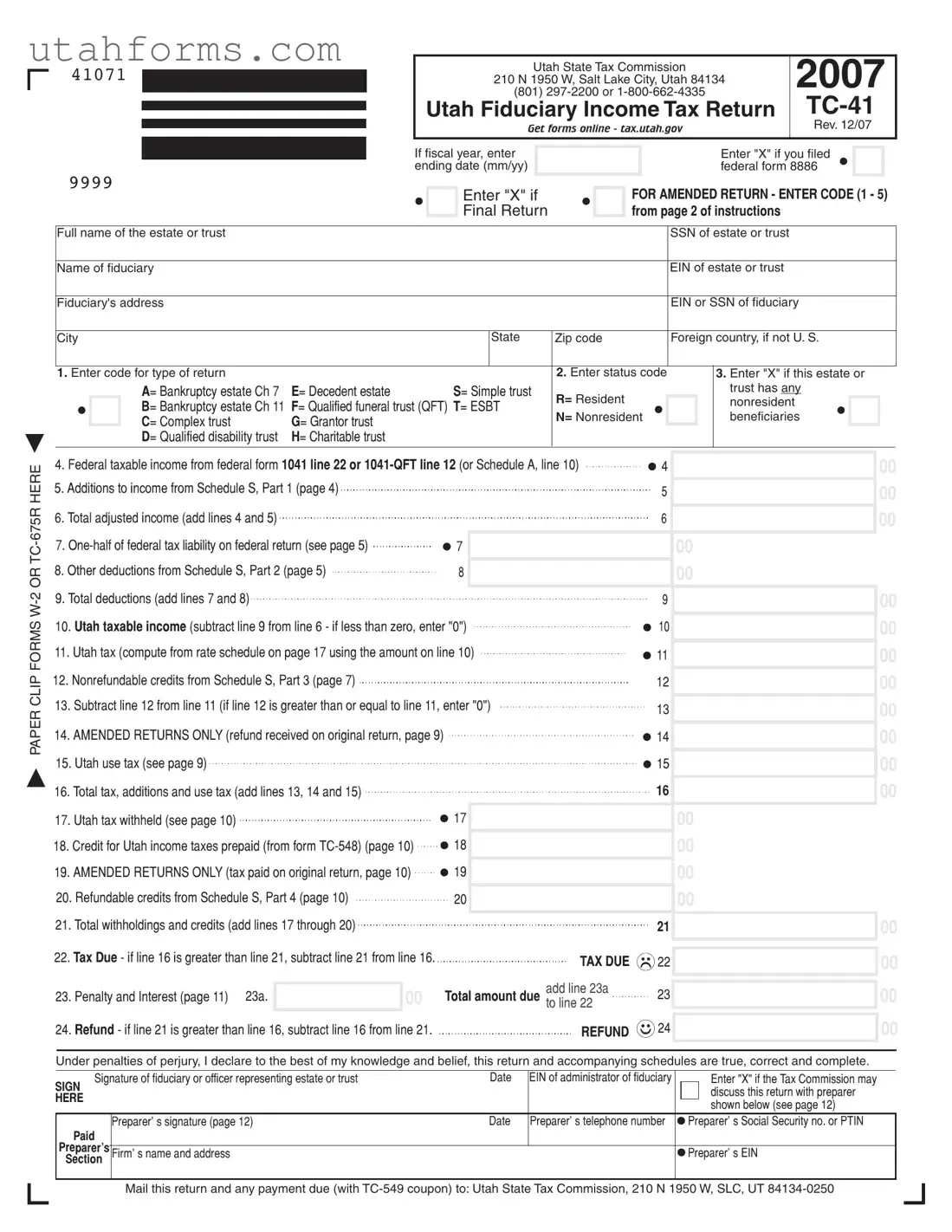

In the realm of estate and trust taxation within Utah, the TC-41 form emerges as a critical document, ensuring compliance with state tax obligations. Administered by the Utah State Tax Commission, this form serves as the Utah Fiduciary Income Tax Return, a pivotal tool for fiduciaries to accurately report income, deductions, and taxes owed by estates or trusts. What sets the TC-41 form apart is its comprehensive design to accommodate various types of estates and trusts, including bankruptcy estates, simple and complex trusts, and charitable trusts, among others. The form also meticulously outlines the procedure for additions to income, deductions, and computation of Utah taxable income based on federal taxable income figures. Moreover, it caters to both resident and nonresident entities, ensuring that fiduciaries can navigate the complexities of state and federal tax alignment efficiently. The inclusion of schedules for nonrefundable and refundable credits, alongside specific provisions for amended returns, highlights the form’s versatility in addressing diverse fiduciary situations. With the Utah Tax Commission providing detailed instructions and the opportunity for professional preparers to engage, the TC-41 form stands as a testament to the state’s commitment to streamlined tax administration for fiduciary entities.

Preview - Utah Tc 41 Form

|

|

|

|

|

|

|

|

|

(801) |

|

|

2007 |

||||||||||

41071 |

|

|

|

|

|

|

Utah State Tax Commission |

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

210 N 1950 W, Salt Lake City, Utah 84134 |

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

Utah Fiduciary Income Tax Return |

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

Get forms online - tax.utah.gov |

|

|

|

Rev. 12/07 |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

If fiscal year, enter |

|

|

|

|

|

|

|

Enter "X" if you filed |

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

ending date (mm/yy) |

|

|

|

|

|

|

|

federal form 8886 |

|

|

||||||

9999 |

|

|

|

|

|

|

Enter "X" if |

|

|

FOR AMENDED RETURN - ENTER CODE (1 - 5) |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

Final Return |

|

|

from page 2 of instructions |

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Full name of the estate or trust |

|

|

|

|

|

|

|

|

|

|

|

SSN of estate or trust |

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Name of fiduciary |

|

|

|

|

|

|

|

|

|

|

|

EIN of estate or trust |

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Fiduciary's address |

|

|

|

|

|

|

|

|

|

|

|

EIN or SSN of fiduciary |

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

City |

|

|

|

|

|

State |

Zip code |

|

|

Foreign country, if not U. S. |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

1. Enter code for type of return |

|

|

|

|

|

|

|

2. Enter status code |

3. Enter "X" if this estate or |

|||||||||||||

|

|

A= Bankruptcy estate Ch 7 |

E= Decedent estate |

|

S= Simple trust |

R= Resident |

|

|

|

|

trust has any |

|

|

|

||||||||

|

|

B= Bankruptcy estate Ch 11 |

F= Qualified funeral trust (QFT) T= ESBT |

|

|

|

|

nonresident |

|

|

|

|

||||||||||

|

|

N= Nonresident |

|

|

beneficiaries |

|

|

|

||||||||||||||

|

|

C= Complex trust |

G= Grantor trust |

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

D= Qualified disability trust |

H= Charitable trust |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PAPER CLIP FORMS

4. Federal taxable income from federal form 1041 line 22 or |

4 |

|

||||

5. Additions to income from Schedule S, Part 1 (page 4) |

|

|

|

5 |

|

|

|

|

|

|

|

|

|

6. Total adjusted income (add lines 4 and 5) |

|

|

|

6 |

|

|

|

|

|

|

|||

|

|

|

|

|||

7. |

|

7 |

|

|

|

|

|

|

|

|

|||

8. Other deductions from Schedule S, Part 2 (page 5) |

|

8 |

|

|

|

|

|

|

|

|

|||

9. Total deductions (add lines 7 and 8) |

|

|

|

|

|

|

|

|

|

9 |

|

||

|

|

|

|

|||

10. Utah taxable income (subtract line 9 from line 6 - if less than zero, enter "0") |

10 |

|

||||

|

||||||

11. Utah tax (compute from rate schedule on page 17 using the amount on line 10) |

11 |

|

||||

12. Nonrefundable credits from Schedule S, Part 3 (page 7) |

|

|

|

12 |

|

|

13. Subtract line 12 from line 11 (if line 12 is greater than or equal to line 11, enter "0") |

13 |

|

||||

|

|

|

|

|

|

|

14. AMENDED RETURNS ONLY (refund received on original return, page 9) |

|

|

14 |

|

||

15. Utah use tax (see page 9) |

|

|

|

15 |

|

|

16. Total tax, additions and use tax (add lines 13, 14 and 15) |

|

|

|

16 |

|

|

|

|

|

|

|||

17. Utah tax withheld (see page 10) |

|

17 |

|

|

|

|

18. Credit for Utah income taxes prepaid (from form |

18 |

|

|

|

||

19. AMENDED RETURNS ONLY (tax paid on original return, page 10) |

19 |

|

|

|

||

|

|

|

||||

20. Refundable credits from Schedule S, Part 4 (page 10) |

|

20 |

|

|

|

|

|

|

|

|

|||

21. Total withholdings and credits (add lines 17 through 20) |

|

|

|

|

|

|

|

|

|

21 |

|

||

22. Tax Due - if line 16 is greater than line 21, subtract line 21 from line 16. |

|

TAX DUE |

22 |

|

||

|

|

|||||

|

|

|

|

|

||

|

|

00 |

|

add line 23a |

23 |

|

|

|

|

|

|||

23. Penalty and Interest (page 11) 23a. |

|

Total amount due to line 22 |

|

|||

|

|

|

||||

24. Refund - if line 21 is greater than line 16, subtract line 16 from line 21. |

|

REFUND |

24 |

|

||

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

Under penalties of perjury, I declare to the best of my knowledge and belief, this return and accompanying schedules are true, correct and complete.

SIGN |

Signature of fiduciary or officer representing estate or trust |

Date |

EIN of administrator of fiduciary |

|

|

Enter "X" if the Tax Commission may |

||

|

|

|

|

|

|

|

discuss this return with preparer |

|

HERE |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

shown below (see page 12) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Preparer' s signature (page 12) |

Date |

Preparer' s telephone number |

|

Preparer' s Social Security no. or PTIN |

|

Paid |

|

|

|

|

|

|

||

Preparer’s |

|

|

|

|

|

|

|

|

|

Firm' s name and address |

|

|

|

Preparer' s EIN |

|||

Section |

|

|

|

|||||

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

Mail this return and any payment due (with

41072

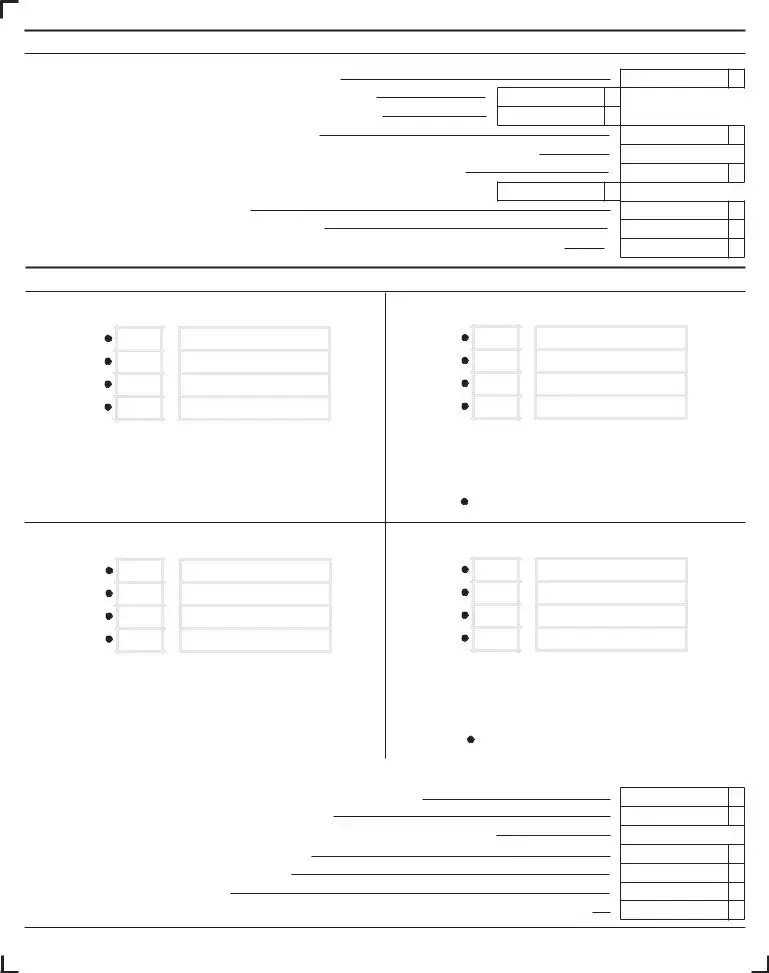

Schedule A – Nonresident Estate or Trust (computation of federal taxable income)

To be completed by all nonresident estates or trusts. |

|

1. Total income from federal form 1041 line 9 or |

|

2. Ordinary income derived from Utah sources (attach schedule - page 13) |

2 |

3. Utah capital gain or (loss) from Utah sources (attach schedule – page 13) |

3 |

4.Total income derived from Utah sources (add lines 2 and 3)

5.Percent of total federal income derived from Utah sources (line 4 divided by line 1 - not greater than 100%)

6.Deductions from federal form 1041or

7. Deductions from federal form 1041 or

8.Allocable amount (line 7 multiplied by line 5)

9.Total deductions allocable to Utah income (add lines 6 and 8)

10. Federal taxable income derived from Utah sources (line 4 less line 9). Enter here and on line 4 on front of form

1

00

00

4

5

6

00

8

9

10

00

00

%

00

00

00

00

Schedule S - Supplemental Schedule

PART 1: ADDITIONS TO INCOME (see codes and descriptions on page 4) |

PART 2: OTHER DEDUCTIONS (see codes and descriptions on page 5) |

Code |

Amount |

Code |

Amount |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

Total additions to income |

|

00 |

Total other deductions |

|

|

00 |

|

|

(enter total on page 1, line 5) |

|

(enter total on page 1, line 8) |

|

|

|

|||

|

|

|

If deducting Native American Income (code 77), write the |

|

|

|

||

|

|

|

enrollment number and tribe code. |

Tribe code |

||||

|

|

|

|

|

|

|||

|

|

|

Enrollment |

|

|

|

|

|

|

|

|

number |

|

|

|

|

|

PART 3: NONREFUNDABLE CREDITS (see codes and descriptions on page 7) |

PART 4: REFUNDABLE CREDITS (see codes and descriptions on page 10) |

||

Code |

Amount |

Code |

Amount |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

Total nonrefundable credits |

|

00 |

|

Total refundable credits |

|

|

00 |

||

(enter total on page 1, line12) |

|

|

(enter total on page 1, line 20) |

|

|

||||

|

|

|

|

|

|

||||

If claiming the Qualified Sheltered Workshop cash contribution |

If claiming the Nonresident Shareholder' s WithholdingTax |

||||||||

credit (code 02), write the Qualified Sheltered Workshop name. |

Credit (code 43), write the S corporation federal ID number. |

||||||||

Name |

|

|

|

|

FEIN |

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PART 5: Credit for fiduciary income tax paid to another state (page 8). Enter code 17 and amount from line 7 below on Part 3, Nonrefundable Credits above. Complete a separate Part 5 for each state for which you are claiming a credit.

1. Total income taxed in state of: |

|

|

1 |

|

|||

2. Total income from federal form 1041 line 9 or |

2 |

||

3. Percent other state income bears to total income (line 1 divided by line 2 - not greater than 100%) |

3 |

||

4. Utah fiduciary tax as computed on line 11 on front of form |

4 |

||

5. Credit limitation (line 4 multiplied by percent on line 3) |

5 |

||

6. Fiduciary tax paid to state listed on line 1 |

6 |

||

7. Credit for fiduciary taxes paid to other state (line 5 or 6, whichever is less) Enter code 17 and credit on Sch. S, Part 3 above. |

7 |

||

00

00

%

00

00

00

00

File Specifications

| Fact | Detail |

|---|---|

| Form Title | Utah Fiduciary Income Tax Return TC-41 |

| Revision Date | December 2007 |

| Contact Information | (801) 297-2200 or 1-800-662-4335 |

| Address for Filing | Utah State Tax Commission, 210 N 1950 W, Salt Lake City, Utah 84134 |

| Website for Forms | tax.utah.gov |

| Special Instructions for Amended Returns | For amended returns, a code (1 - 5) must be entered to indicate the reason for amendment. |

| Requirement for Federal Form 8886 | Indicate with an "X" if federal form 8886 has been filed. |

| Type of Entity Codes | Includes codes for bankruptcy estate, decedent estate, trusts, and qualified disability trust among others. |

| Governing Law | Administered under the laws governing the State of Utah's tax regulations. |

| Special Sections for Nonresident Estates or Trusts | Includes instructions for calculating income and deductions derived from Utah sources. |

How to Write Utah Tc 41

When it's time to deal with the Utah TC-41 Fiduciary Income Tax Return, it's essential to approach the task methodically to ensure accuracy and compliance. This form is designed for the reporting of income, deductions, and taxes for estates or trusts. Filling it out correctly helps the Utah State Tax Commission assess the correct tax obligations. The following steps provide guidance on how to efficiently complete the Utah TC-41 form.

- Start by gathering all necessary documentation, including federal tax returns and any relevant income statements for the estate or trust.

- Enter the full name of the estate or trust along with its Social Security Number (SSN) or Employer Identification Number (EIN) at the top of the form.

- Provide the name, address, and EIN or SSN of the fiduciary responsible for the estate or trust.

- If this is an amended return, mark the "X" box provided and enter the amendment code (1-5) that applies to your situation.

- Indicate the fiscal year ending date (mm/yy) if applicable, and if the federal form 8886 was filed by marking the "X" box.

- Select the appropriate code for the type of return from the list provided in step 1 on the form and enter it in the specified field.

- Enter the status code in step 2 as provided in the instructions based on the estate or trust's specific situation.

- If the estate or trust has any nonresident beneficiaries, mark the "X" box in step 3 to indicate this.

- Calculate and enter the federal taxable income from the corresponding line on the federal form 1041 or 1041-QFT.

- Add any necessary additions to income as detailed in Schedule S, Part 1, and enter the total in step 5.

- Add lines 4 and 5 to find the total adjusted income and record this amount in step 6.

- Enter one-half of the federal tax liability as specified in the form instructions.

- Include other deductions from Schedule S, Part 2, and enter the total amount of deductions.

- Subtract total deductions from total adjusted income to determine the Utah taxable income, ensuring to enter "0" if the result is less than zero.

- Use the rate schedule provided on the form to calculate the Utah tax based on the taxable income and enter this amount.

- Document nonrefundable credits from Schedule S, Part 3, and subtract this from the Utah tax to determine the adjusted tax owed.

- If applicable, include the refund received on the original return, Utah use tax, total tax, withholdings, credits, and any amounts for amended returns.

- Calculate the total withholdings and credits, then determine whether there is a tax due or a refund owed by following the instructions for lines 22 and 24.

- If there is any penalty and interest due, calculate and enter the total amount.

- The fiduciary or an officer representing the estate or trust must sign and date the form. If prepared by someone other than the fiduciary, the preparer's information must also be included.

- Finally, ensure all necessary documentation is attached, including any required schedules or forms, such as W-2s or TC-675R forms for withholdings.

- Mail the completed form, along with any payment due, to the Utah State Tax Commission at the address provided on the form.

By carefully following these steps, the fiduciary can complete the Utah TC-41 form accurately and in compliance with Utah tax laws, ensuring that the estate or trust's tax obligations are met in a timely manner.

Frequently Asked Questions

Frequently Asked Questions about Utah TC-41 Form

- What is the Utah TC-41 Form used for?

The Utah TC-41 form, also known as the Utah Fiduciary Income Tax Return, is a document that must be filed by fiduciaries of estates and trusts. It's used to report income, deductions, gains, losses, and taxes due for the estate or trust. Filing this form helps ensure that the fiduciary correctly reports the entity's annual financial activity to the Utah State Tax Commission.

- Who needs to file a Utah TC-41 Form?

Anyone acting as a fiduciary for an estate or trust in Utah is required to file the TC-41 form. This includes estates of deceased persons, bankruptcy estates, and various types of trusts, such as simple trusts, complex trusts, and grantor trusts. Filing is necessary whether the estate or trust is resident or nonresident, as long as it has income derived from Utah sources or is subject to Utah state taxes.

- How does one determine if amendments are needed on a previously filed TC-41?

To determine if amendments are necessary for a previously filed TC-41 form, fiduciaries should review the original return for any inaccuracies or changes to the estate or trust's income, deductions, or tax liability. If discrepancies are found or if there have been adjustments to the federal return that affect state tax liability, an amended return may be needed. The form has a specific section for amendments where one can mark an "X" for an amended return and enter the appropriate amendment code (1-5) based on the changes being made.

- What are the key sections of the TC-41 form that require careful attention?

- Type of Return and Status Codes: These codes identify the type of entity filing the return and its tax status, which can affect tax computation.

- Income and Deductions: Accurately reporting income and qualifying deductions is crucial for calculating the correct tax liability. This includes both federal taxable income and any additions or deductions specific to Utah.

- Nonrefundable and Refundable Credits: Filing for applicable state credits can reduce the amount of tax owed. It’s important to review available credits and eligibility requirements.

- Penalties and Interest: If the form is filed late or taxes are underpaid, penalties and interest may apply. Calculating and including these amounts ensures compliance and avoids further issues with the state tax commission.

Attention to these sections will help in correctly filing the TC-41 form and complying with Utah state tax laws.

Common mistakes

When filling out the Utah TC-41 form, people commonly make a range of mistakes that can affect their tax returns. These errors can lead to delays, audits, or improper tax assessments. It's vital to approach this document with attention to detail to ensure accuracy and compliance.

- Incorrectly entering tax identification numbers: Both the Social Security Number (SSN) of the estate or trust and the Employer Identification Number (EIN) of the fiduciary are crucial. Misentering these numbers can cause significant processing delays.

- Choosing the wrong type of return: The form requires specifying the type of entity filing the return (such as a bankruptcy estate, decedent estate, or various trusts). Incorrect selection can result in improper tax calculations or filings.

- Failing to report nonresident beneficiaries: This is particularly important for entities that have any nonresident beneficiaries. Neglecting to mark this can impact the taxation and withholding requirements.

- Omitting federal taxable income information or inaccuracies in reporting it: As the Utah tax calculation begins with federal taxable income, any inaccuracies or omissions here will ripple through the entire return.

- Incorrect additions and deductions: Both adding income not reported on the federal return and claiming deductions require careful attention. Mistakes in these sections can either inflate the tax due or decrease the refund unjustly.

- Overlooking nonrefundable and refundable credits: Taxpayers often miss claiming eligible credits, such as those for taxes paid to other states or for contributions to qualified sheltered workshops. This oversight can lead to a higher tax bill than necessary.

- Errors in calculating the tax due, refund amounts, or penalties: Accuracy in these final calculations is critical. Overpayments and underpayments can both be costly, and inaccuracies might trigger audits.

To ensure accuracy on the Utah TC-41 form, it's advisable to:

- Double-check all identification numbers and codes entered.

- Review the definitions and requirements for each type of return and beneficiary status.

- Ensure all income is accurately reported and calculated using the correct federal and state forms as a reference.

- Verify all credits claimed for eligibility and accurately calculate these amounts.

- Consult the instructions for the form or seek professional advice if any uncertainties arise.

By avoiding these common mistakes, filers can help ensure their Utah fiduciary tax returns are correctly and efficiently processed, minimizing the risk of errors or an audit.

Documents used along the form

When preparing the Utah TC-41 form, a Fiduciary Income Tax Return, several additional forms and documents might be required to ensure a complete and accurate filing. These documents support various sections of the TC-41 by providing detailed information that might not be fully captured within the primary form itself. Understanding these additional forms will streamline the tax preparation process and comply with Utah State Tax Commission requirements.

- TC-547: This document serves as the Payment Voucher for filing fees associated with the TC-41. Taxpayers use it to facilitate the payment process when mailing their return, ensuring that funds are correctly applied to their account.

- TC-675R: The Statement of Withholding for Utah is crucial for estates or trusts that have withholding tax from various income sources. It provides detailed information on taxes already withheld, which is necessary for completing line 17 of the TC-41 form.

- TC-548: Filing Extension Request is used if the fiduciary realizes they cannot file the TC-41 by the deadline and need an extension. This form does not extend the time to pay taxes due but prevents late filing penalties.

- Schedule S: Supplemental Schedule is part of the TC-41 package and is used to report additions to income, other deductions, nonrefundable, and refundable credits that affect Utah taxable income. It ensures that all necessary adjustments are made to federal taxable income for state tax purposes.

- Form 1041: U.S. Income Tax Return for Estates and Trusts is a federal form that the TC-41 instructions frequently reference. Information from Form 1041 helps to populate various lines on the TC-41, especially Line 4 concerning federal taxable income.

- Schedule K-1 (1041): Beneficiary’s Share of Income, Deductions, Credits, etc., is used to report a beneficiary's share of the estate's or trust's income, deductions, and credits. Although it is a federal form, insights from Schedule K-1 are crucial for preparing both federal and state fiduciary income tax returns accurately.

Each document plays a pivotal role in the overall tax preparation process for an estate or trust filing in Utah. These forms ensure the comprehensive reporting of income, deductions, credits, and payments associated with the fiduciary's financial activities within the tax year. Tax professionals should review each applicable document thoroughly to ensure compliance and accuracy in filing the Utah TC-41 form.

Similar forms

The IRS Form 1041, U.S. Income Tax Return for Estates and Trusts, shares similarities with the Utah TC-41 form as both are used to report income, deductions, and credits of estates and trusts. These forms ensure the appropriate taxation of entities under their respective jurisdictions, with the IRS Form 1041 covering federal tax obligations while the TC-41 addresses state-specific requirements in Utah.

Form 1041-QFT, U.S. Income Tax Return for Qualified Funeral Trusts, like the TC-41, is designed for a specific type of trust, focusing on those established per a death to fulfill the financial aspects of funerals. Although catering to distinct trust types, both forms serve the key role of reporting income and applying relevant tax codes to ensure the proper handling of tax liabilities within their designated frameworks.

The Schedule K-1 (Form 1041), Beneficiary's Share of Income, Deductions, Credits, etc., is another document akin to the Utah TC-41. This schedule distributes income and deductions to beneficiaries from the estate or trust, akin to how TC-41 collects and reports income for taxation purposes. Each document plays a critical part in the transparent reporting and tax obligation fulfillment for estates and trusts.

Form 706, United States Estate (and Generation-Skipping Transfer) Tax Return, while primarily used for reporting the transfer of deceased individuals' estates, has parallels with the TC-41 in its role of managing tax responsibilities associated with estates. Although focusing more on the transfer and inheritance aspects, both forms are integral in the estate planning and taxation process.

Form 709, United States Gift (and Generation-Skipping Transfer) Tax Return, is designed for reporting gifts that exceed the annual threshold, similar to how the TC-41 form reports income for trusts and estates. Both are critical in ensuring transparency and compliance with tax obligations stemming from wealth transfer activities.

The Form 990, Return of Organization Exempt from Income Tax, required for non-profit organizations, shares commonalities with the TC-41, as both involve the reporting of income and expenses to tax authorities. While serving different entities, each form ensures adherence to tax laws and the proper administration of tax-related responsibilities.

The Form 8821, Tax Information Authorization, allows third parties to access tax information, reflecting the TC-41's provision for a preparer to discuss return details with the Utah Tax Commission. This feature in both forms emphasizes the importance of representation and professional assistance in managing tax affairs.

Form 4506-T, Request for Transcript of Tax Return, like the section in TC-41 that addresses amended returns, offers parties the ability to access previously filed tax information, which is useful for amendments or deeper tax analysis. Both functionalities support tax compliance and the thorough management of tax records.

The Form SS-4, Application for Employer Identification Number (EIN), parallels the TC-41 in its foundational role for trust or estate taxation. Just as the SS-4 provides an essential identifier for tax purposes, the TC-41 utilizes the EIN for estates and trusts to track and manage their tax obligations within Utah.

Lastly, the Form W-2, Wage and Tax Statement, and accompanying schedules mentioned in the TC-41, highlight the collaborative nature of tax documentation gathering and reporting. Both the W-2's employee income reporting and the TC-41's income aggregation for estates and trusts underscore the meticulous approach required for accurate tax compliance.

Dos and Don'ts

When preparing the Utah TC-41, Fiduciary Income Tax Return, it's crucial to be meticulous in order to avoid common mistakes that could lead to delays or errors in processing. Here are seven key dos and don'ts to consider:

- Do ensure all information is accurate and complete. Double-check the estate or trust’s full name, SSN or EIN, the fiduciary's name, and address details are entered correctly.

- Do mark the appropriate boxes clearly, such as indicating if it is an amended return or if the estate or trust has any nonresident beneficiaries.

- Do attach all necessary documents, including Forms W-2 or TC-675R, securely with a paper clip as instructed on the form.

- Do accurately calculate the Utah taxable income, tax due, and refundable amounts by carefully following the instructions provided within the form and the accompanying schedules.

- Do not forget to sign and date the form. The preparer’s signature, if applicable, along with the date and contact information, should also be included to validate the filing.

- Don't overlook the addition to income and other deductions sections. It is essential to report all relevant financial details accurately to avoid underpayment penalties.

penalties of perjury that the information provided is true, correct, and complete. This declaration is made by signing the form at the designated section.

By adhering to these guidelines, you can ensure that the Utah TC-41 form is filled out correctly and processed efficiently by the Utah State Tax Commission. Remember, accuracy, completeness, and adherence to instructions are key to a smooth filing process.

Misconceptions

Understanding tax forms can sometimes be challenging, and misconceptions are common. Here's a look at four common misconceptions about the Utah TC-41 form, which is used for fiduciary income tax returns in Utah:

- Only for Trusts and Estates with Utah Source Income: It's a common misunderstanding that the Utah TC-41 form is only required for trusts and estates that have income sourced directly from Utah. While it is crucial for those with Utah source income, it’s also required for all fiduciary entities that are subject to Utah state tax laws, regardless of the income source.

- Filing Amended Returns Is Complicated: Some might think that filing an amended TC-41 form is a complicated process that requires extensive backtracking and additional documentation. However, the form provides clear instructions on how to report changes from the original return by marking it as amended and entering the appropriate codes. Detailed instructions ensure fiduciaries can correct or update their filing status or income with ease.

- No Need to Report Federal Tax Information: There's a misconception that you don't need to provide any information related to your federal tax return when filing a Utah TC-41 form. Contrary to this belief, federal taxable income figures and other relevant federal tax information are required as a part of the TC-41 filing process to accurately assess the Utah tax liability.

- The Form Doesn't Address Nonresident Beneficiaries: Another misunderstanding is thinking the TC-41 form does not consider the status of nonresident beneficiaries of trusts or estates. In reality, the form requires fiduciaries to indicate whether the estate or trust has nonresident beneficiaries. This information impacts how the income is taxed and what credits or deductions might be applicable.

Clearing up these misconceptions helps in understanding the requirements and processes associated with the Utah TC-41 form, ensuring proper compliance with Utah state tax obligations. Always refer to the official instructions or consult with a tax professional when preparing tax documents to make sure you are following current guidelines and rules.

Key takeaways

Filling out the Utah TC-41 form is an essential process for trustees and fiduciaries in Utah to ensure proper state income tax returns for estates and trusts. Understanding the key aspects of this form can streamline the process, avoid common mistakes, and ensure compliance with Utah state tax laws. Here are some pivotal takeaways:

- Identify the Type and Status of the Return: When starting with the form, make sure to correctly identify the type of return (e.g., estate, trust, bankruptcy estate) and the status code. This first step is crucial as it sets the foundation for how the rest of the form should be completed.

- Report Federal Taxable Income Accurately: The federal taxable income figures need to be transferred from the federal form 1041 or 1041-QFT to the TC-41. Accuracy here is essential as it impacts the computation of Utah taxable income.

- Additions and Deductions: Carefully review Schedule S parts 1 and 2 for additions to income and other deductions. Mistakes in this section can lead to incorrect tax calculations and potential issues with the Utah State Tax Commission.

- Understanding Credits: The form allows for various nonrefundable and refundable credits. These can significantly impact the final tax liability and, in some cases, result in a refund. Specific credits, such as those for taxes paid to other states, require detailed attention.

- Penalties and Interest: If you owe taxes, it's important to also calculate any penalties and interest correctly to avoid further notices or bills from the tax commission. This part often requires careful reading of the instructions and may need additional guidance.

- Signatures are Mandatory: The form must be signed by the fiduciary or officer representing the estate or trust. An unsigned form can lead to processing delays and potential penalties. Additionally, if a tax preparer was used, their information must also be included.

Lastly, ensuring that the form is sent to the correct address with any payment due is critical. Late filings or payments can result in penalties and interest charges. Navigating the complexities of the Utah TC-41 form with care can ensure compliance and potentially minimize the estate or trust's tax liabilities.

Common PDF Templates

Utah Professional Licensing - A mechanism for businesses to officially communicate their exempt status, aligning with Utah regulatory norms.

Utah Dmv Forms - The Utah TC-301 form is an essential starting point for those venturing into the bonded motor vehicle industry in Utah, ensuring businesses comply with state regulations.

Utah State Withholding - The TC-51 form helps Utah evaluate if a business meets the criteria for collecting sales or use tax in the state.