Fill Out Your Utah Seller Financing Addendum Form

In navigating the complex terrain of real estate transactions in Utah, the Seller Financing Addendum form plays a pivotal role, especially when traditional financing mechanisms are not an option. This document, which becomes a part of the overarching Real Estate Purchase Contract (REPC), outlines the specific terms under which the seller of a property extends credit to the buyer, facilitating a smoother transactional process. Key elements include the identification and agreement on the credit documents, detailing the principal amount, interest rate, payment schedule, and any balloon payments or additional terms that might be applicable. Furthermore, it addresses responsibility for property taxes, insurance, and homeowners association dues, designating how these expenses are to be paid. The form also stipulates how payments under the seller financing arrangement should be made, outlines the protocol for late payments or prepayment, and details the conditions under which a due-on-sale clause might be triggered. Additionally, it mandates certain buyer disclosures related to financial information and grants the seller the right to review and possibly reject the buyer based on creditworthiness before moving forward. Title insurance requirements, disclosure of tax identification numbers for IRS reporting, and the mechanism for accepting, countering, or rejecting the addendum further encapsulate the comprehensive nature of this document. With an effective date signaling its mandatory use, this form stands as a testament to the evolving landscape of real estate transactions in Utah, aiming to provide transparency and security for both buyer and seller in seller-financed deals.

Preview - Utah Seller Financing Addendum Form

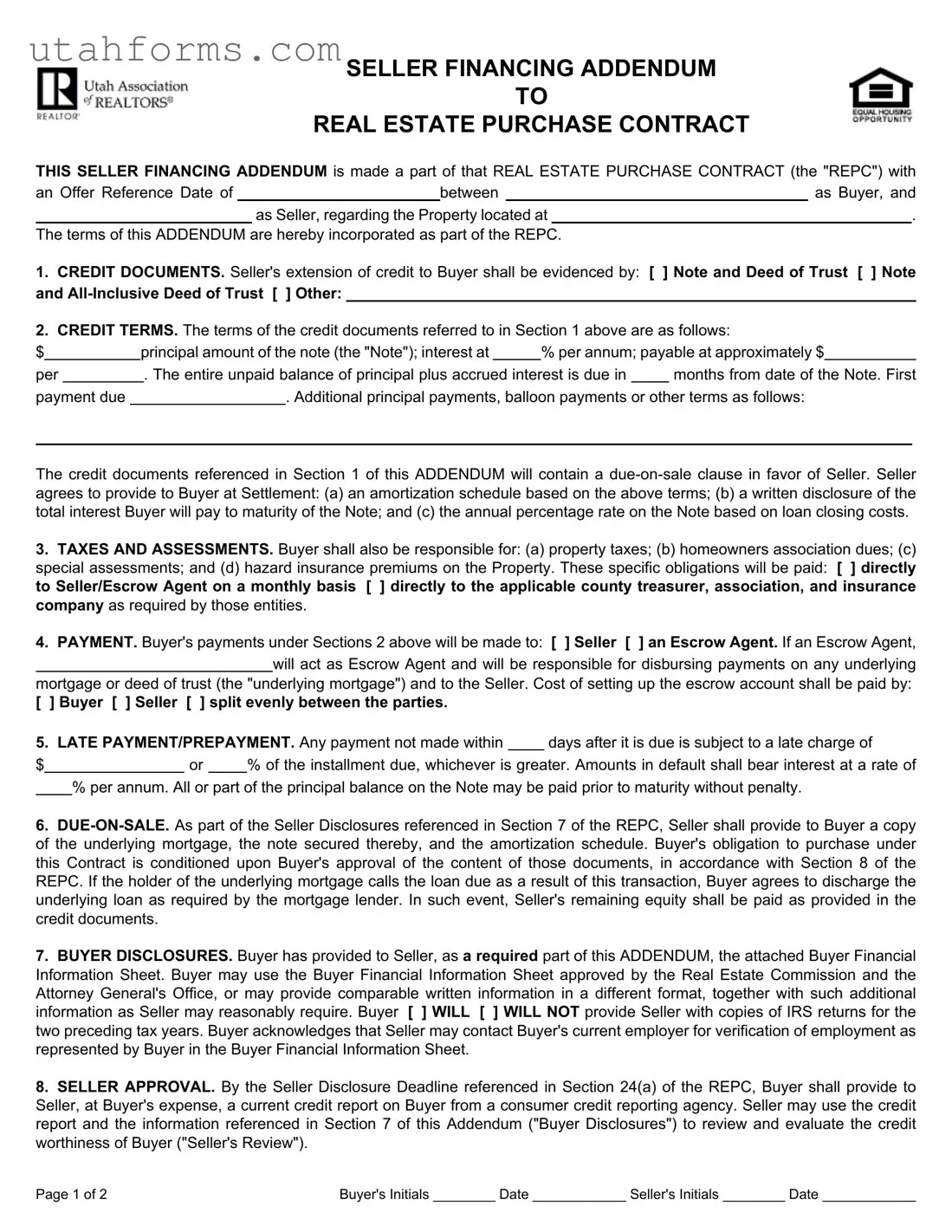

SELLER FINANCING ADDENDUM

TO

REAL ESTATE PURCHASE CONTRACT

THIS SELLER FINANCING ADDENDUM is made a part of that REAL ESTATE PURCHASE CONTRACT (the "REPC") with

an Offer Reference Date of |

|

|

between |

|

as Buyer, and |

||

|

|

as Seller, regarding the Property located at |

|

. |

|||

|

|

|

|

|

|||

The terms of this ADDENDUM are hereby incorporated as part of the REPC. |

|

|

|||||

1.CREDIT DOCUMENTS. Seller's extension of credit to Buyer shall be evidenced by: [ ] Note and Deed of Trust [ ] Note and

2.CREDIT TERMS. The terms of the credit documents referred to in Section 1 above are as follows:

$ |

|

|

principal amount of the note (the "Note"); interest at |

|

% per annum; payable at approximately $ |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

per |

|

|

|

. The entire unpaid balance of principal plus accrued interest is due in |

|

months from date of the Note. First |

|||||

payment due |

|

|

|

. Additional principal payments, balloon payments or other terms as follows: |

|||||||

The credit documents referenced in Section 1 of this ADDENDUM will contain a

3.TAXES AND ASSESSMENTS. Buyer shall also be responsible for: (a) property taxes; (b) homeowners association dues; (c) special assessments; and (d) hazard insurance premiums on the Property. These specific obligations will be paid: [ ] directly to Seller/Escrow Agent on a monthly basis [ ] directly to the applicable county treasurer, association, and insurance company as required by those entities.

4.PAYMENT. Buyer's payments under Sections 2 above will be made to: [ ] Seller [ ] an Escrow Agent. If an Escrow Agent,

will act as Escrow Agent and will be responsible for disbursing payments on any underlying mortgage or deed of trust (the "underlying mortgage") and to the Seller. Cost of setting up the escrow account shall be paid by:

[ ] Buyer [ ] Seller [ ] split evenly between the parties.

5. LATE PAYMENT/PREPAYMENT. Any payment not made within |

|

days after it is due is subject to a late charge of |

||||

$ |

|

or |

|

% of the installment due, whichever is greater. Amounts in default shall bear interest at a rate of |

||

%per annum. All or part of the principal balance on the Note may be paid prior to maturity without penalty.

6.

7.BUYER DISCLOSURES. Buyer has provided to Seller, as a required part of this ADDENDUM, the attached Buyer Financial Information Sheet. Buyer may use the Buyer Financial Information Sheet approved by the Real Estate Commission and the Attorney General's Office, or may provide comparable written information in a different format, together with such additional information as Seller may reasonably require. Buyer [ ] WILL [ ] WILL NOT provide Seller with copies of IRS returns for the two preceding tax years. Buyer acknowledges that Seller may contact Buyer's current employer for verification of employment as represented by Buyer in the Buyer Financial Information Sheet.

8.SELLER APPROVAL. By the Seller Disclosure Deadline referenced in Section 24(a) of the REPC, Buyer shall provide to Seller, at Buyer's expense, a current credit report on Buyer from a consumer credit reporting agency. Seller may use the credit report and the information referenced in Section 7 of this Addendum ("Buyer Disclosures") to review and evaluate the credit worthiness of Buyer ("Seller's Review").

Page 1 of 2 |

Buyer's Initials ________ Date ____________ Seller's Initials ________ Date ____________ |

8.1Seller Review. If Seller determines, in Seller's sole discretion, that the results of the Seller's Review are unacceptable, Seller may either: (a) no later than the Due Diligence Deadline referenced in Section 24(b) of the REPC, cancel the REPC by providing written notice to Buyer, whereupon the Earnest Money Deposit shall be released to Buyer without the requirement of further written authorization from Seller; or (b) no later than the Due Diligence Deadline referenced in Section 24(b), resolve in writing with Buyer any objections Seller has arising from Seller's Review.

8.2Failure to Cancel or Resolve Objections. If Seller fails to cancel the REPC or resolve in writing any objections Seller has arising from Seller's Review, as provided in Section 8.1 of this ADDENDUM, Seller shall be deemed to have waived the Seller's Review.

9.TITLE INSURANCE. Buyer [ ] SHALL [ ] SHALL NOT provide to Seller a lender's policy of title insurance in the amount of the indebtedness to the Seller, and shall pay for such policy at Settlement.

10.DISCLOSURE OF TAX IDENTIFICATION NUMBERS. By no later than Settlement, Buyer and Seller shall disclose to each other their respective Social Security Numbers or other applicable tax identification numbers so that they may comply with federal laws on reporting mortgage interest in filings with the Internal Revenue Service.

To the extent the terms of this ADDENDUM modify or conflict with any provisions of the REPC, including all prior addenda and counteroffers, these terms shall control. All other terms of the REPC, including all prior addenda and counteroffers, not modified

by this ADDENDUM shall remain the same. [ |

] Seller |

[ ] Buyer shall have until |

|

: |

|

[ ] AM [ ] PM Mountain Time |

|||

on |

|

|

(Date), to accept the terms of this SELLER FINANCING ADDENDUM in accordance with Section 23 of |

||||||

the REPC. Unless so accepted, the offer as set forth in this SELLER FINANCING ADDENDUM shall lapse. |

|||||||||

|

|

|

|

|

|

|

|

|

|

[ ] Buyer [ |

] Seller Signature |

(Date) |

(Time) |

|

|

|

Social Security Number |

||

[ ] Buyer [ ] Seller Signature |

(Date) |

(Time) |

Social Security Number |

ACCEPTANCE/COUNTEROFFER/REJECTION

CHECK ONE:

[ ] ACCEPTANCE: [ ] Seller [ ] Buyer hereby accepts the these terms.

[] COUNTEROFFER: [ ] Seller [ ] Buyer presents as a counteroffer the terms set forth on the attached ADDENDUM NO.

[] REJECTION: [ ] Seller [ ] Buyer rejects the foregoing SELLER FINANCING ADDENDUM.

(Signature) |

(Date) |

(Time) (Signature) |

(Date) |

(Time) |

THIS FORM APPROVED BY THE UTAH REAL ESTATE COMMISSION AND THE OFFICE OF THE UTAH ATTORNEY GENERAL, EFFECTIVE AUGUST 27, 2008. AS OF

JANUARY 1, 2009, IT WILL REPLACE AND SUPERCEDE THE PREVIOUSLY APPROVED VERSION OF THIS FORM.

Page 2 of 2 |

Buyer's Initials ________ Date ____________ Seller's Initials ________ Date ____________ |

File Specifications

| Fact | Description |

|---|---|

| Document Title | Utah Seller Financing Addendum to Real Estate Purchase Contract |

| Purpose | Incorporates terms of seller financing into the Real Estate Purchase Contract (REPC) |

| Content | Details on credit documents, payment terms, responsibilities for taxes and assessments, late payment/prepayment conditions, and more. |

| Governing Law | Regulated by provisions and requirements set forth by the Utah Real Estate Commission and the Office of the Utah Attorney General. |

| Key Features | Includes options for documenting credit, details on payment amounts and schedule, responsibilities on taxes, and insurance. |

| Due-on-Sale Clause | Specifies that the credit documents will contain a due-on-sale clause in favor of the Seller. |

| Modification and Conflict | Clarifies that terms in this addendum will override any conflicting terms in the REPC and past addenda. |

| Approval Process | Describes the process for Seller's review of buyer's financial information and outlines potential outcomes based on this review. |

How to Write Utah Seller Financing Addendum

Completing the Utah Seller Financing Addendum form is a crucial step in the process of a real estate purchase where the seller is providing financing to the buyer. This addendum modifies and complements the main Real Estate Purchase Contract (REPC), outlining the terms under which the seller extends credit to the buyer for purchasing the property. It's essential for both parties, the buyer and the seller, to accurately fill out this addendum to ensure clear understanding and agreement on the seller financing terms. Here are the steps to correctly complete the form:

- Start by entering the Offer Reference Date of the REPC to which this addendum applies.

- Fill in the names of the Buyer and the Seller as stated in the REPC.

- Specify the address of the Property being purchased under "regarding the Property located at".

- In Section 1, select the appropriate option(s) to indicate how the seller's extension of credit to the buyer will be evidenced (Note and Deed of Trust, Note and All-Inclusive Deed of Trust, Other).

- Under Section 2, fill in the principal amount of the note, the interest rate per annum, the payment amount, and the payment frequency. Additionally, specify the due date for the first payment and detail any additional terms like balloon payments.

- Detail the responsibilities of the buyer regarding taxes and assessments in Section 3, choosing whether these will be paid directly to the Seller/Escrow Agent on a monthly basis or directly to the respective entities.

- Identify where the buyer's payments will be made under Section 4, choosing either Seller or an Escrow Agent, and stating the name of the Escrow Agent if applicable.

- Specify any late charge policies in Section 5, including the amount or percentage for late charges and interest rates on defaulted amounts.

- Under Section 6, acknowledge the due-on-sale clause and the condition upon buyer's approval of the underlying mortgage documents.

- Complete Section 7 by outlining the financial disclosures the buyer has provided, including whether the buyer will provide copies of IRS returns for the two preceding tax years and any employer verification procedures.

- In Section 8, mention by what date a current credit report on the Buyer will be provided to the Seller and how objections based on the Seller's Review are to be addressed.

- Indicate in Section 9 whether the Buyer will provide to Seller a lender's policy of title insurance and who will pay for it.

- Both parties must disclose their Social Security Numbers or other tax identification numbers by Settlement in Section 10.

- Finally, indicate by what date and time the terms of this addendum need to be accepted by marking the appropriate boxes and filling in the specific date and time.

- Both the Buyer and Seller must sign and date the form, including their Social Security Numbers where indicated.

- Indicate the agreed action at the end of the form: Acceptance, Counteroffer, or Rejection by marking the appropriate box and signing and dating.

Upon completion, this detailed form ensures that all specifics regarding seller financing are formally agreed upon and documented, contributing to a transparent and smooth transaction for both the property buyer and seller.

Frequently Asked Questions

Frequently Asked Questions about the Utah Seller Financing Addendum Form

What is the Utah Seller Financing Addendum?

The Utah Seller Financing Addendum is a document that becomes part of a Real Estate Purchase Contract (REPC), outlining the terms under which the seller provides financing to the buyer for purchasing property. It details the credit documents, terms of credit, responsibilities for taxes and assessments, payment methods, and conditions related to late or prepayments, among other things.

What are "credit documents" as referred to in the Addendum?

Credit documents provide evidence of the seller's extension of credit to the buyer. These may include a Note and Deed of Trust, an All-Inclusive Deed of Trust, or other forms agreed upon by both parties. These documents specify the amount borrowed, interest rates, payment schedules, and other credit terms.

How are taxes and assessments handled in seller financing?

Under seller financing, the buyer is responsible for property taxes, homeowners association dues, special assessments, and hazard insurance premiums. These costs can be paid directly to the seller or an escrow agent monthly or directly to the entities like county treasurers or insurance companies as required.

What happens if a payment is late?

If a payment is not made within the specified days after its due date, a late charge will apply, which is either a fixed amount or a percentage of the installment due. Defaulted amounts will accrue interest at a predetermined annual rate. The agreement allows for principal balance prepayment without penalty, with specific terms outlined for such scenarios.

What is a "Due-on-Sale" clause?

A "Due-on-Sale" clause is part of the credit documents that allows the seller to demand full repayment of the loan if the buyer decides to sell the property. This clause ensures that the seller has the option to be paid off before the property changes hands again.

What are "Buyer Disclosures"?

Buyer Disclosures include financial information provided by the buyer to the seller as part of the addendum. This includes a financial information sheet approved by the Real Estate Commission and the Attorney General's Office, IRS returns for the two preceding tax years (if required), and possibly verification of employment. This information helps the seller to evaluate the buyer's creditworthiness.

How does Seller Approval work?

By the Seller Disclosure Deadline, the buyer must provide the seller with a current credit report. The seller reviews this report and other buyer disclosures to assess the creditworthiness of the buyer. If the seller finds the results unsatisfactory, they may cancel the REPC or work out any objections with the buyer. Failing to resolve objections implies the seller's acceptance of the buyer's financial standing.

Common mistakes

When parties are filling out the Utah Seller Financing Addendum form, mistakes can happen. This form, crucial for establishing the terms of seller financing in real estate transactions, requires careful attention to detail. Unfortunately, errors in completing this form can lead to misunderstandings, delays, and legal complications.

One common mistake is inaccurately documenting the credit terms specified in Section 2. This section outlines the principal amount, interest rate, payment schedule, and the duration of the loan. Ensuring these figures are accurately captured is fundamental. Misrepresenting the interest rate or the principal amount, even by a small margin, can significantly affect the repayment terms, potentially causing financial strain for the buyer or yielding less profit for the seller than intended.

Another area prone to errors is the specification of responsibilities regarding taxes, assessments, and insurance payments in Section 3. Participants often overlook the importance of clearly defining who pays for what and how these payments are to be made. Failing to specify that the buyer is responsible for property taxes, homeowners association dues, special assessments, and hazard insurance premiums can create confusion and disputes after the sale has closed.

Incorrectly setting up the terms for late payments or prepayments in Section 5 is another frequent mistake. It's crucial to clearly define the late payment charges and the conditions under which prepayment penalties do or do not apply. When these details are vague or incorrectly filled out, it can lead to unnecessary conflicts between the seller and buyer regarding the expected penalties or rewards for early repayment.

- Omitting or inaccurately detailing the setup and responsibility for the escrow account in Section 4 can lead to significant issues. It's essential to designate who will manage the escrow account and outline the allocation of setup costs.

- Failing to provide or correctly complete the Buyer Financial Information Sheet as required in Section 7 often leads to a lack of critical information for evaluating the buyer's creditworthiness.

- Not properly addressing or misunderstanding the due-on-sale clause presented in Section 6 can result in unexpected financial obligations. This clause requires careful consideration, especially in how it relates to the underlying mortgage and its impact on the transaction if the loan is called due.

In addition to these specific issues, a general mistake is not thoroughly reviewing the entire document before submission. This overconfidence can lead to missed checkboxes, unsigned sections, and inaccuracies in important details like names, addresses, and Social Security numbers. Such oversights can invalidate the agreement or necessitate legal corrections, delaying the transaction. It's paramount for all involved parties to review each section carefully before finalizing the addendum.

To avoid these mistakes, parties should consider consulting with legal professionals or real estate experts familiar with the Utah Seller Financing Addendum. Doing so can help ensure the agreement accurately reflects the terms of the deal and is legally sound, preventing future disputes or financial losses.

Documents used along the form

In real estate transactions, particularly those involving seller financing in Utah, the Utah Seller Financing Addendum form plays a pivotal role. Such an arrangement can offer flexibility to both buyers and sellers, allowing for unique financing terms that might not be possible with traditional lending sources. However, to ensure the process is comprehensive and legally sound, several other forms and documents are often used alongside the Utah Seller Financing Addendum form. These additional documents help to clarify the terms of the deal, protect the interests of both parties, and comply with state and federal laws.

- Real Estate Purchase Contract (REPC): This foundational document outlines the basic terms of the real estate transaction, including the purchase price, property description, and closing details. The Utah Seller Financing Addendum is attached to and modifies this contract.

- Buyer Financial Information Sheet: This form is mentioned directly in the Utah Seller Financing Addendum. It provides the seller with information about the buyer's financial situation, assisting in the evaluation of the buyer's creditworthiness.

- Amortization Schedule: This document details how the loan payments are applied to the principal and interest over the life of the loan. It is provided by the seller to the buyer, as stated in the addendum, offering a clear schedule of payments and how they affect the loan balance over time.

- Credit Report Authorization: The seller uses this form to obtain the buyer's consent to pull their credit report. This is an essential step for assessing the creditworthiness of the buyer, as mentioned in the Seller's Review section of the addendum.

- Deed of Trust or Mortgage: Depending on the specific agreement and legal requirements, either a deed of trust or a mortgage is used to secure the loan on the property. This legal document is critical for protecting the seller's interest by creating a lien on the property.

- Title Insurance Policy: The buyer often provides the seller with a lender's title insurance policy to protect against any defects in the property title. This requirement is outlined in the addendum, ensuring the seller's security in the property until the loan is paid in full.

- Seller Disclosure Statements: Required by law, these documents provide the buyer with essential information about the property's condition and history, including any known defects or issues that could affect the property's value or livability.

Utilizing these documents in conjunction with the Utah Seller Financing Addendum ensures a comprehensive approach to seller-financed real estate transactions. Each plays a distinct role in clarifying terms, verifying information, and securing the interests of both buyer and seller, thereby facilitating a smoother transaction and helping to prevent future disputes. As always, consulting with a real estate attorney can provide additional insights and ensure all legal requirements are met.

Similar forms

The Real Estate Purchase Contract (REPC) closely resembles the Utah Seller Financing Addendum form in its core function of facilitating the sale of real estate. However, while the Seller Financing Addendum focuses specifically on the terms under which the seller will finance the purchase for the buyer, the REPC covers a broader range of details regarding the property transaction. These include, but are not limited to, identification of the parties, description of the property, purchase price, and the settlement date. The Addendum serves as an integral component of the REPC when seller financing is involved, specifying the credit terms and obligations directly tied to the purchase agreement.

The Promissory Note is another document with significant parallels to the Utah Seller Financing Addendum. It evidence the borrower's (in this context, the buyer's) promise to repay a loan to the lender (the seller). Both documents detail the amount of the loan, interest rate, repayment schedule, and the consequences of late payments. However, the Promissory Note is a standalone financial document, whereas the Seller Financing Addendum incorporates these financial terms into the broader context of a real estate transaction.

A Deed of Trust or Mortgage often accompanies seller-financed real estate transactions, serving a complementary role to the Seller Financing Addendum by securing the loan with the property itself. This ensures that if the buyer defaults on the loan, the seller has the legal right to foreclose on the property to recoup the owed amount. The key difference lies in the scope: the Deed of Trust or Mortgage focuses solely on the security interest in the property, whereas the Addendum outlines the full array of financing terms agreed upon by the buyer and seller.

Amortization Schedules are closely linked to the information found in the Seller Financing Addendum, providing a detailed breakdown of each payment over the life of the loan and how it applies to both the principal and interest. While the Addendum mentions that an amortization schedule will be provided, the schedule itself is a separate document that visually represents the repayment plan, showcasing the gradual reduction of the loan balance over time.

The Disclosure of Loan Closing Costs, often a requirement in real estate transactions involving financing, shares similarities with the Seller Financing Addendum through its role in ensuring transparency about the financial aspects of the transaction. It details the closing costs associated with securing a loan, including but not limited to, lending fees, title insurance, and processing fees. The Addendum, while not a detailed list of such costs, stipulates that the annual percentage rate on the Note is based on these loan closing costs, making the two documents complementary in understanding the financial implications of the transaction.

The Buyer Financial Information Sheet, referred to within the Seller Financing Addendum, serves as a critical document providing the seller with insight into the buyer's financial health and creditworthiness. This can include details such as income, debt, and assets, which helps the seller make an informed decision about extending credit. While the Seller Financing Addendum outlines the terms under which financing is offered, the Buyer Financial Information Sheet provides the financial context for those terms, making both documents crucial to the seller-financed sales process.

Finally, the Escrow Agreement for a seller-financed purchase shares similarities with the Utah Seller Financing Addendum in its execution of financial and contractual obligations. This agreement involves a third party that holds and regulates the payment of the funds required for the transaction based on the agreed terms between the buyer and seller. While the Seller Financing Addendum specifies terms regarding payments to, and possibly through, an Escrow Agent, the Escrow Agreement itself governs the escrow arrangement in detail, ensuring that all financial transactions between the buyer and seller occur in a timely and transparent manner.

Dos and Don'ts

When filling out the Utah Seller Financing Addendum form, it's crucial to pay attention to both the dos and don'ts to ensure accuracy and compliance with legal requirements. Below are key points to consider:

Do:- Review the entire form thoroughly before starting to fill it out to understand all the provisions and how they relate to your agreement.

- Ensure all financial terms, such as the principal amount of the note, interest rate, payment schedule, and any balloon payments, are clearly and correctly entered as agreed upon between the buyer and seller.

- Verify the accuracy of the property description, including the address and any legal description, to ensure it matches the property being financed.

- Include an amortization schedule, total interest disclosure, and annual percentage rate as required in the addendum to provide complete financial details to the buyer.

- Complete the Buyer Disclosures section accurately, attaching the required Buyer Financial Information Sheet and any additional documentation as necessary.

- Sign and date the form within the specified acceptance period as indicated in the acceptance section to formalize the agreement.

- Consult with a real estate professional or attorney if you have any questions or uncertainties about the addendum or its implications.

- Skip any sections or leave blank spaces unless specifically instructed, as incomplete documents can lead to misunderstanding or legal issues.

- Alter the terms of the financing after signing without a written agreement from both parties, as any changes to the financing terms require proper documentation and approval.

- Fail to provide the buyer with a copy of the underlying mortgage, the note, and the amortization schedule, as this is crucial for transparency and compliance with the due-on-sale clause.

- Ignore the deadline for the seller's review and approval of the buyer's creditworthiness and financial information, as failing to meet this deadline could affect the validity of the addendum.

- Omit the disclosure of Social Security Numbers or tax identification numbers by the settlement date, which is necessary for IRS reporting requirements.

- Assume verbal agreements are enough for any amendments or additions to the financing terms; always document changes in writing and have both parties sign off.

- Forget to check that both buyer and seller initials are on all pages and that all required signatures and dates are included before submission.

Misconceptions

Many people have misunderstandings about the Utah Seller Financing Addendum form. Let's clarify some of the most common misconceptions:

- Seller financing is always more expensive for the buyer. This is not necessarily true. While interest rates may be higher than traditional bank loans, the overall financial arrangements can be more flexible and negotiable between the buyer and seller, potentially making it a financially viable option for many buyers.

- The form is only used for residential properties. Although commonly associated with residential real estate transactions, the Utah Seller Financing Addendum can be utilized for the sale and purchase of commercial properties as well, where the seller agrees to finance part of the purchase price.

- Buyer financial information is not always required. On the contrary, the form explicitly states that the buyer must provide financial information to the seller. This requirement is crucial for the seller to evaluate the creditworthiness of the buyer. The form even allows the seller to request IRS returns from the last two tax years.

- All seller-financed transactions include a balloon payment. While the addendum allows for the inclusion of balloon payments or additional principal payments, they are not mandatory components of every seller-financed deal. Terms are negotiable and can be structured to meet the specific needs of both the buyer and the seller.

- The seller cannot cancel the contract if they find the buyer's credit unsatisfactory. Actually, the seller has the right to cancel the real estate purchase contract if, upon review of the buyer's credit and financial information, they find it unsatisfactory. This must be done by a specified due diligence deadline.

- Failure of the buyer to approve the seller's credit will automatically void the transaction. The truth is, the addendum lays out conditions that allow the transaction to be canceled if the buyer disapproves of the seller's financial documents. However, it also provides mechanisms for resolving objections, suggesting that cancellation is not automatic or inevitable.

Understanding these nuances is crucial for both buyers and sellers to navigate their transactions effectively. Misconceptions can lead to unrealistic expectations and outcomes that do not serve the interests of either party. Always review the forms and consult with a professional to ensure a clear understanding of the terms and obligations.

Key takeaways

When engaging in property transactions involving seller financing in Utah, it is imperative to accurately complete the Utah Seller Financing Addendum form. This document supplements the Real Estate Purchase Contract (REPC), incorporating crucial terms that govern the seller-financed portion of the purchase. Here are key takeaways to ensure successful usage and compliance:

- The Addendum is integral to the REPC: The terms detailed within the Seller Financing Addendum become an essential part of the REPC. Both buyer and seller should thoroughly review this addendum to understand the specific financing details, such as credit documents, payment terms, and obligations related to taxes and insurance.

- Outline of credit documents: The form specifies the type of credit documents required, such as a Note and Deed of Trust or an All-Inclusive Deed of Trust. Understanding these options and selecting the appropriate document type is crucial for establishing a clear and legally binding financing agreement.

- Clear definition of payment terms: Terms including the principal amount, interest rate, payment schedule, and any provisions for balloon payments or additional principal payments are explicitly stated. This clarity prevents confusion and ensures that both parties have aligned expectations.

- Responsibility for taxes, assessments, and insurance: The buyer's responsibilities towards property taxes, homeowners association dues, special assessments, and hazard insurance premiums are enumerated. Whether these are paid directly to the relevant entities or through the seller/escrow agent is specified, highlighting the importance of regular payments to avoid potential issues.

- Provisions for late payment and prepayment: The addendum details any fees associated with late payments and clarifies the buyer's rights regarding prepayment of the principal balance. These provisions help in maintaining a fair and transparent relationship between the buyer and seller.

Overall, the Utah Seller Financing Addendum form plays a pivotal role in transactions where the seller provides financing to the buyer. By meticulously filling out this form and adhering to its terms, both parties can ensure a smooth and agreeable sale process, with protections in place to address any financial contingencies that may arise.

Common PDF Templates

Utah Vehicle Title Transfer - Strengthens state oversight on vehicle and vessel registration by requiring a detailed inspection of identification numbers.

Survivorship Affidavit Utah - It is an essential tool for anyone looking to contest a vehicle impound decision in Utah effectively.

Utah State Withholding Form - The form requires details such as FEIN/SSN, tax period, and the applicant’s contact information, ensuring a smooth refund process.